Is Honda Civic Considered a Sports Car For Insurance? See Pricing!

Is Honda Civic Considered a Sports Car For Insurance? Usually no. A standard Honda Civic (LX, EX, Sport) is classified as a compact sedan for insurance. However, the Civic Si may be rated as a sport compact, and the Civic Type R is often treated as a high-performance model depending on the insurer’s risk data.

In this guide, we clarify how insurers classify each trim from older models through 2026 versions, using real underwriting logic rather than guesswork.

Do Insurance Companies Classify the Honda Civic as a Sports Car?

In most cases, standard Civic trims are not classified as sports cars. They are rated as compact passenger vehicles.

However, classification changes when the model has performance upgrades or a high accident frequency.

How insurers typically classify trims:

| Civic Trim (1990 to 2026) | Typical Insurance Category | Risk Level |

| DX / LX / EX | Compact sedan | Low–Moderate |

| Sport / Touring | Compact sedan | Moderate |

| Si (2006 to 2026) | Sport compact | Moderate–High |

| Type R (2017 to 2026) | Performance vehicle | High |

Most base models are rated like a Toyota Corolla or Mazda3. The Si and Type R get flagged differently because they attract younger drivers and have higher repair costs.

Does the Civic Si Count as a Sports Car for Insurance?

Sometimes. The Civic Si (2006–2026 models) has a turbocharged engine in newer generations and produces around 200 horsepower. That is not exotic, but insurers look at who buys it and how it is driven.

In real underwriting data, the Si often lands in a sport compact category. That means slightly higher premiums than a Civic LX, but usually not as high as a Mustang GT or Subaru WRX.

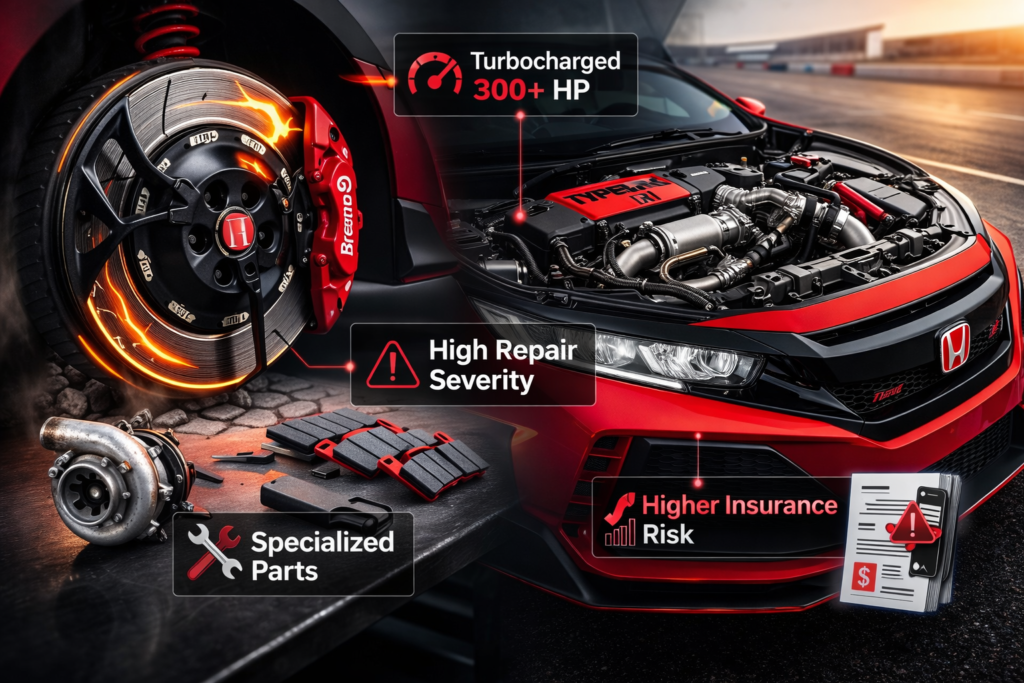

Is the Civic Type R Treated as a High-Performance Vehicle by Insurers?

Yes, in most cases. The Civic Type R (2017 to 2026) makes over 300 horsepower and uses specialized brakes, tires, and body panels. That increases repair severity, a big factor in insurance pricing.

Why insurers rate the Type R higher:

- 300+ horsepower turbocharged engine

- Expensive performance parts

- Higher theft interest in some regions

- Younger performance-focused buyers

Read Guide: Throttle Response Tuning Honda Accord Drive By Wire Improvement?

Why Can Honda Civic Insurance Be Higher Than Expected?

Even when it is not labeled a sports car, Civic insurance can surprise people.

Older Civics (especially 1998–2015 models) were among the most stolen vehicles in North America. High theft claim frequency raises comprehensive coverage rates.

Add to that:

- High modification rates

- Dense urban ownership

- Younger driver demographics

That is why a Civic can cost more than expected even without V8 power.

For example, I have seen two drivers in the same city pay very different premiums for the same Civic. One was a 19-year-old with a Sport trim. The other was a 38-year-old with an LX. Same car family, very different risk profiles.

How Do Insurers Decide Whether a Car Is a Sports Car?

Insurance companies do not rely on marketing terms. They use rating systems.

Here is what actually matters:

- ISO symbol rating (vehicle risk score)

- Historical accident frequency

- Average repair cost per claim

- Horsepower and engine type

- Driver profile trends

A 2026 Civic Hybrid, for example, is rated lower risk than a 2023 Type R even though both are new. Underwriters price behavior patterns, not just badges.

In 2025–2026, many insurers adjusted rating tiers for turbocharged compact cars. Instead of labeling them sports cars, some now place them into separate performance rating tiers based on claim severity ratios and loss ratios. That change affects Civic Si and Type R premiums more than base trims.

Actuarial data examine loss ratios and claim severity ratios to determine a vehicle’s symbol factor, which ultimately places it in a specific rating tier.

Verisk/ISO’s Vehicle Series Rating explanation.

Does Body Style (Coupe vs Sedan) Affect Civic Insurance Rates?

Yes, especially on older models. Two-door Civic coupes (1990 to 2020) often carried slightly higher premiums. Historically, couples have shown higher accident rates among younger drivers. Sedans are statistically safer in insurance data pools.

The 2026 Civic lineup is sedan-only in most markets, which simplifies classification and slightly stabilizes premiums compared to older coupe years.

Back in the early 2000s, coupe Civics were frequently modified, raced, and crashed at higher rates than sedans. That historical claim frequency still influences how older two-door models are rated today.

Also Read: Do Honda Civics Have Leather Seats?

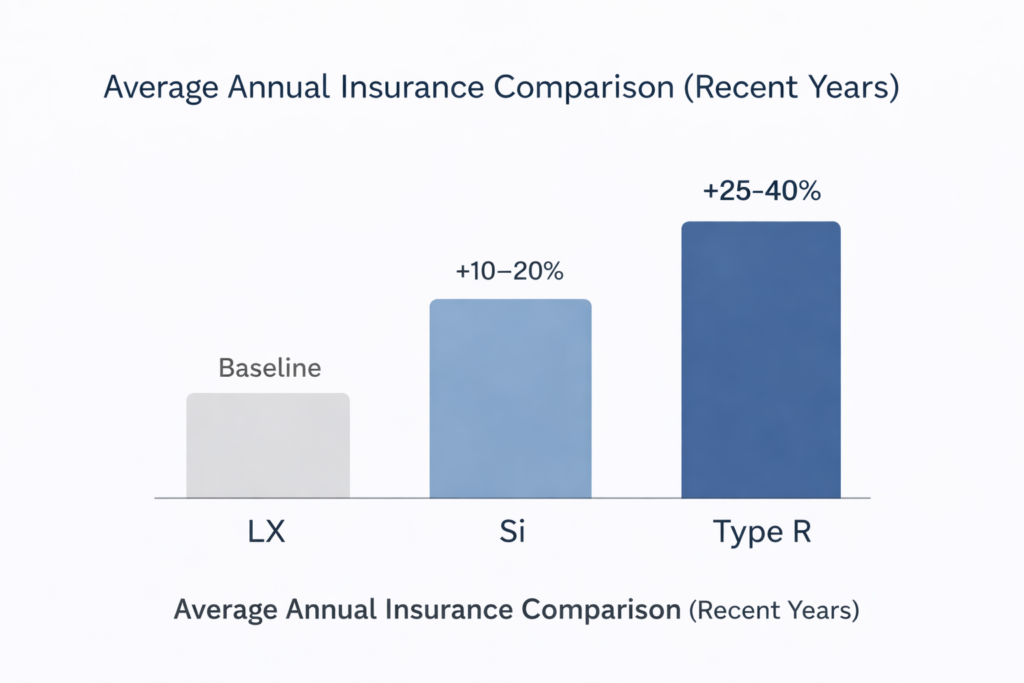

How Much More Does a Civic Si or Type R Cost to Insure?

On average, performance trims cost more but not extreme-sports-car levels.

| Model (Recent Years) | Avg Annual Insurance (US est.) | Compared to Base Civic |

| Civic LX | $1,400 to $1,700 | Baseline |

| Civic Si | $1,600 to $1,950 | +10–20% |

| Civic Type R | $1,900 to $2,400+ | +25–40% |

Rates vary by state, age, and driving record. A 22-year-old driver will see a bigger gap than a 40-year-old with a clean history.

Does Your State Affect How the Civic Is Classified for Insurance?

Yes, pricing varies heavily by location.

States with:

- High theft rates

- Dense traffic

- Higher medical claim costs

…will produce higher Civic premiums.

Also, some insurers separate performance trims more aggressively in urban markets. A Civic Si in California may be priced differently than the same car in Ohio.

There is no federal sports car label. It is insurer-defined.

How Can You Lower Insurance Costs on a Civic Si or Type R?

Start with the basics:

- Increase deductible

- Bundle home and auto

- Use telematics (safe-driving tracking)

- Avoid aftermarket performance mods

In 2026, many insurers will reward usage-based programs. If you drive calmly, you can offset the performance trim penalty.

A clean driving record matters more than the badge.

What Most Drivers Get Wrong About Civic Insurance?

Many drivers assume horsepower alone defines a sports car. In insurance underwriting, that is rarely true. Theft frequency, modification trends, and repair cost volatility often matter more than raw engine output. That is why a 200-hp Civic Si can cost more to insure than a heavier V6 sedan.

When Is a Honda Civic Considered a Sports Car for Insurance?

A standard Honda Civic is not considered a sports car for insurance. The Civic Si may be treated as a sport compact by some insurers. The Civic Type R is often classified as a performance vehicle based on horsepower, repair costs, and risk data.

So, if you are asking, “Is Honda Civic considered a Sports Car for Insurance?” The honest answer is trim-dependent, data-driven, and risk-based.

Insurance companies do not price hype. They price history.

FAQs:

Is the Honda Civic Si considered a sports car for insurance?

Yes. Many insurers classify the Civic Si as a sport compact due to its turbo performance and higher-risk data.

Is the Civic Type R treated as a high-performance vehicle?

Yes. The Type R is commonly rated as a performance car because of its 300+ horsepower and higher repair costs.

Is a base Honda Civic LX considered a sports car?

No. Standard Civic trims like LX and EX are classified as compact sedans, not sports cars.

Why does Civic insurance cost more in some states?

Insurance varies by theft rates, accident data, and local claim costs, not just the model itself.

Does horsepower alone determine sports car classification?

Horsepower matters, but insurers also review accident history, repair severity, and driver demographics.

Conclusion:

Whether a Honda Civic is considered a sports car for insurance depends on the trim and risk profile, not the nameplate alone. Base models remain affordable to insure, while performance variants like the Si and Type R carry higher premiums due to underwriting data. Insurance pricing is built on statistics, not assumptions. Understanding that difference helps you make smarter buying and budgeting decisions.